The amortised cost of a financial asset or financial liability is the amount

- at which the financial asset or financial liability is measured at initial recognition,

- minus principal repayments,

- plus or minus the cumulative amortisation using the effective interest method of any difference between that initial amount and the maturity amount, and

- minus any reduction (directly or through the use of an allowance account) for impairment or un-collectability.

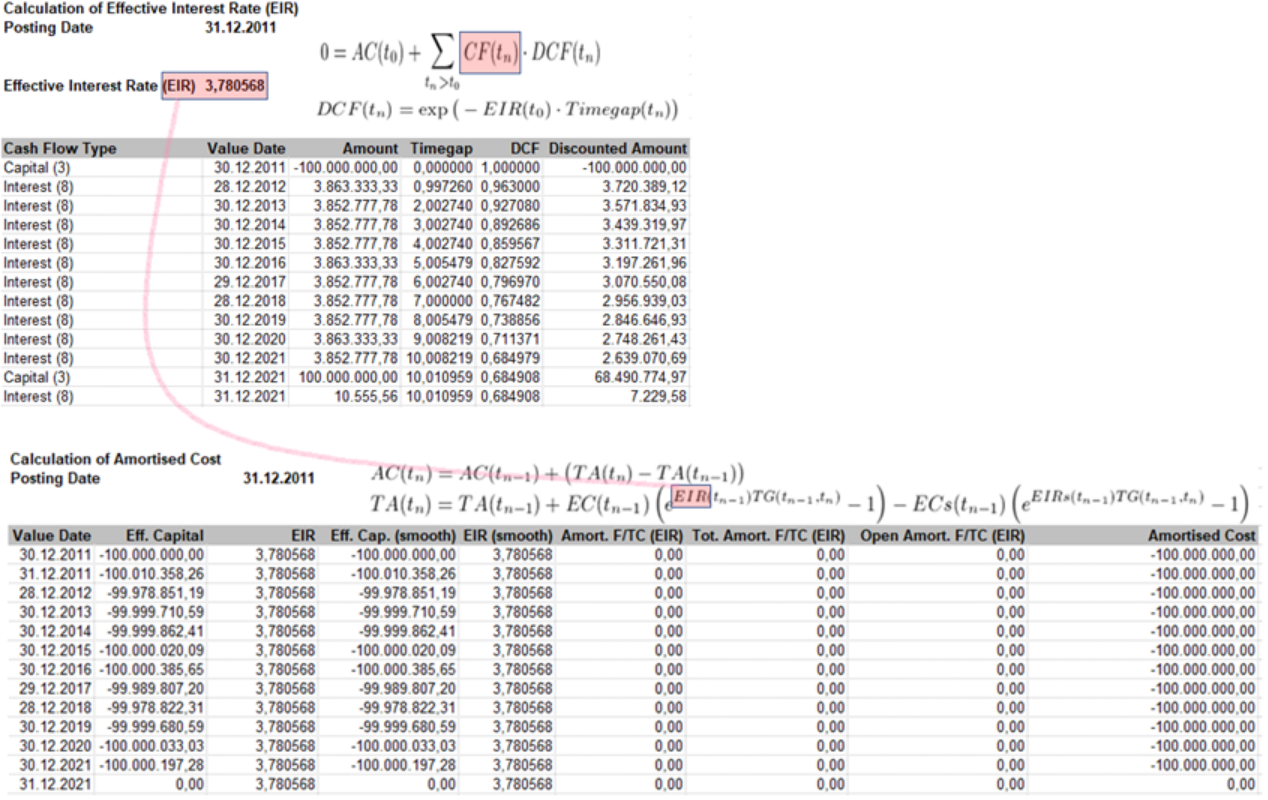

In view of the definition of the amortised cost, the following formula is used for its calculation:

![]()

- At further payment dates, the amortised cost equals the amortised cost of the previous payment date, plus the difference of the current cumulative total amortisation TA(tn) and the one from the previous payment date TA(tn-1), plus possible principal repayments PR(tn):

![]()

The cumulative total amortisation TA(tn) of payment date tn is defined by

![]()

- The effective capital EC(tn) of payment date tn is defined as the negative of the sum of all future cash flows discounted by the effective interest rate:

![]()

In order to check the calculation of the effective capital in Excel exports of the calculation analyser, the following equivalent recursive formula for the effective capital is useful:

![]()

- The smoothing effective interest rate EIRs is calculated exaxctly like the EIR – only all cash flows of premiums/discounts/charges/transaction costs are ignored in the calculation.

- Analogously, the smoothing effective capital ECs is calculated exactly like the EC – only the EIRs are used instead of the EIR.

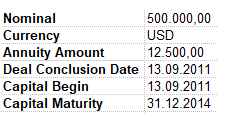

The following annuity loan is considered:

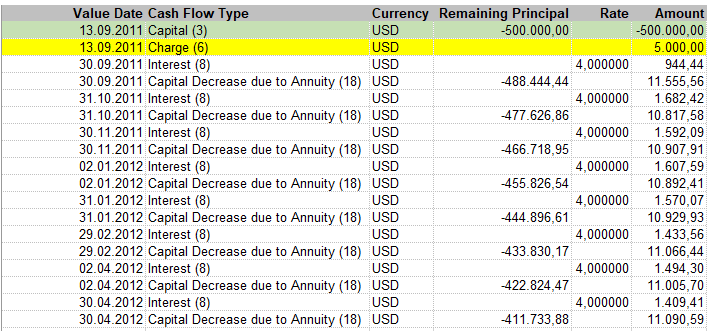

Initially, there is also a charge of 5000 USD. Hence, the first cash flows for the deal are as follows:

Applying the calculation method described, the calculation of the amortised cost of the deal starts as follows: