...

| Expand | |||||

|---|---|---|---|---|---|

| |||||

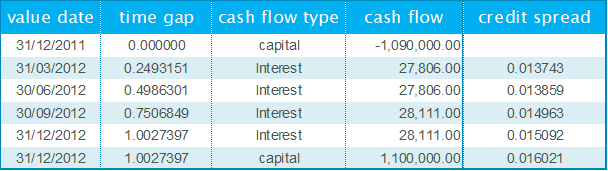

The credit spread is the risk premium on the market interest rate which depends on the credit rating of the counterparty. It represents the yield difference between sound government-issued bonds and corporate bonds. Example: One deal with customer rating Aaa and one deal with customer rating Ba are considered.The market interest rate is 4% and the funding spread 0.5%. The credit spread for companies with an Aaa rating is 0.25% and the credit spread for companies with a Ba rating is 0.75%. Then the interest rate for the first deal will be 4.75% (= 4% + 0.5% + 0.25%) and the interest rate for the second deal will be 5.25% (= 4% + 0.5% + 0.75%). Based on the raw statistics delivered, for example probabilities of default, credit spreads can be derived by the solution via various tools and methodologies. Alternatively, credit spreads can be delivered from market data providers, front office or risk system resources. The following situations may result in a change in credit spreads:

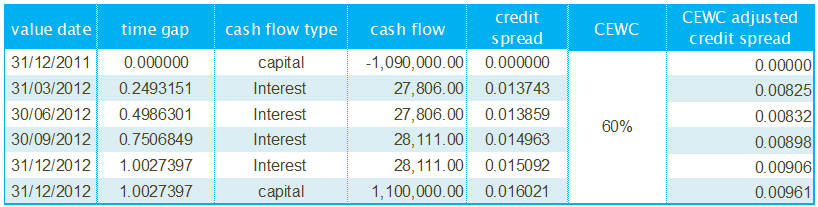

Collateral Enhancement Weighting Coefficient The collateral enhancement weighting coefficient (CEWC) determines a reduction in the credit spread of a loan due to collateral instruments and describes the percentage by which the collateralisation reduces the risk of an asset. It is a constant between 0 and 1. For a loan perfectly covered by collateral, the CEWC will be 0. If a loan has no collateral at all, the CEWC equals 1. In general, if a deal is collateralised with p% of its outstanding payment, its corresponding CEWC is (100-p)%. In order to determine a CEWC, the following approaches can be used:

|

| Expand | |||||

|---|---|---|---|---|---|

| |||||

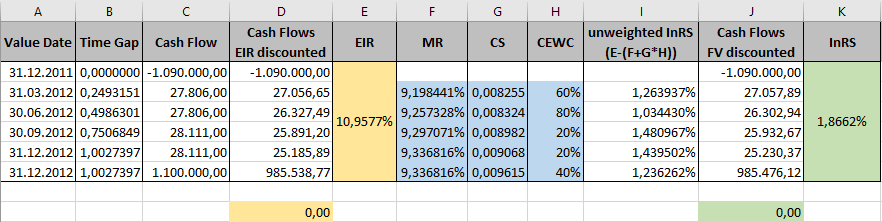

The initial residual spread (InRS) is a constant value which is calculated as a residual amount on the deal conclusion date. The InRS is calculated so that, on the deal conclusion date, the fair value of the deal on the start date corresponds to the cost of purchase, i.e. on the deal start date, the sum of the discounted cash flows corresponds to the cost of purchase. When the “price” of a financial product (e.g. a loan or a bond) is determined by the bank, several components are taken into account, e.g.

Due to the following reason, knowing the InRS is important in the accounting world:

Hence, the InRS can be understood as the profit margin of a deal. Basically, the idea of the InRS is that it will be calculated only once at the beginning of the lifetime of a financial instrument. However, the following situations can be seen as comparable to the “birth” of a new financial instrument so that the InRS has to be recalcualted:

|

...

| Expand | ||

|---|---|---|

| ||

When the full fair value/hedge fair value is calculated using the discounted cash flow method, so-called forward exchange rates are generally required for deals with cash flows in different currencies. The reason for this logical necessity is to carry out netting [1] of cash flows for deals with cash inflows and outflows and then to discount the netted/balanced cash flows on the valuation date. This is of particular importance since the plus/minus sign of the netted amount is used to decide if the credit spread of the counterparty (for incoming payments) or the bank's credit spread (for outgoing payments) is to be used. It is also relevant if it has been configured in the basic configuration that the in/out rule is to be used for the determination of the market interest rate. (See the chapter "In/Out Rule" in the chapter "Calculation of the Discount Factors".) Thus these cash flows are first weighted using forward exchange rates and then discounted using the discounted cash flow method. Taking simple arbitrage considerations into account, forward exchange rates between two currencies can be calculated directly from the spot exchange rates for currencies and the risk-free market interest curves for the individual currencies. Let us assume that, at the point in time t, the forward exchange rates between the EUR and USD are to be calculated using the spot exchange rate between the EUR and USD and the current yield curves for the two currencies. For the forward exchange rate at the point in time tn, for arbitrage reasons, the following must apply:

Figure: Arbitrage Considerations for Forward Exchange Rates The forward exchange rate is calculated as follows:

|